Should You Accept Microsoft’s Voluntary Retirement Program Offering?

Microsoft recently announced its first-ever Voluntary Retirement Program (VRP), and an estimated 8,750 employees now face a life-changing decision.

To make an informed choice, you need to understand the "Rule of 70," quantify the value of the benefits, and see how this fits into your long-term financial plan.

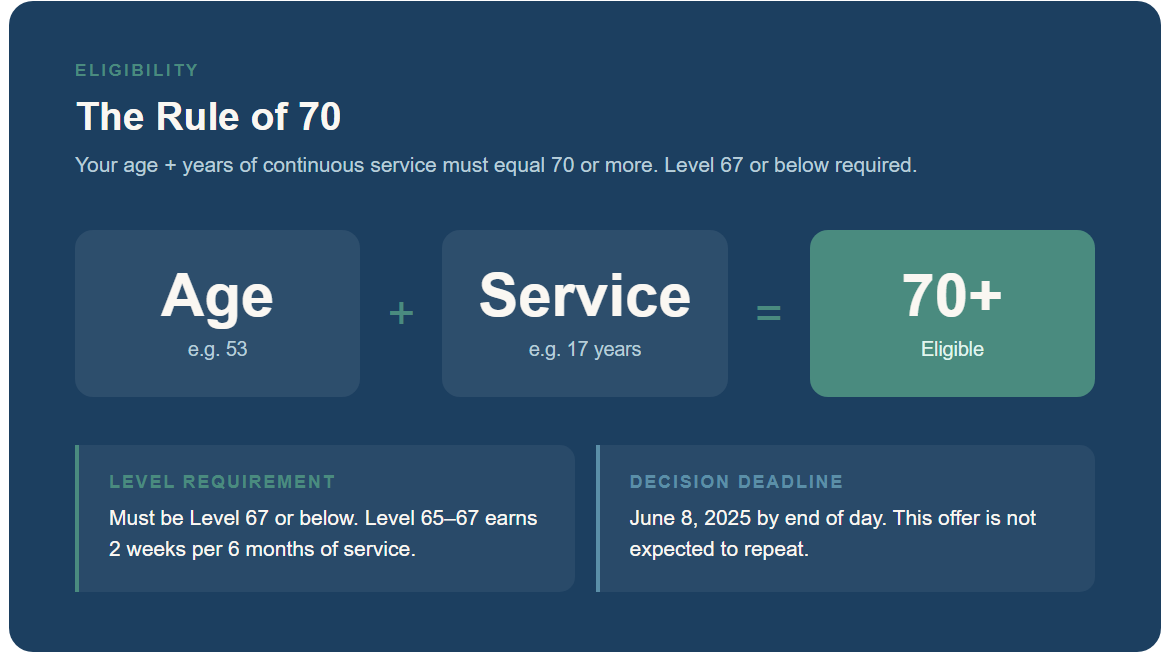

Are You Eligible? (The Rule of 70)

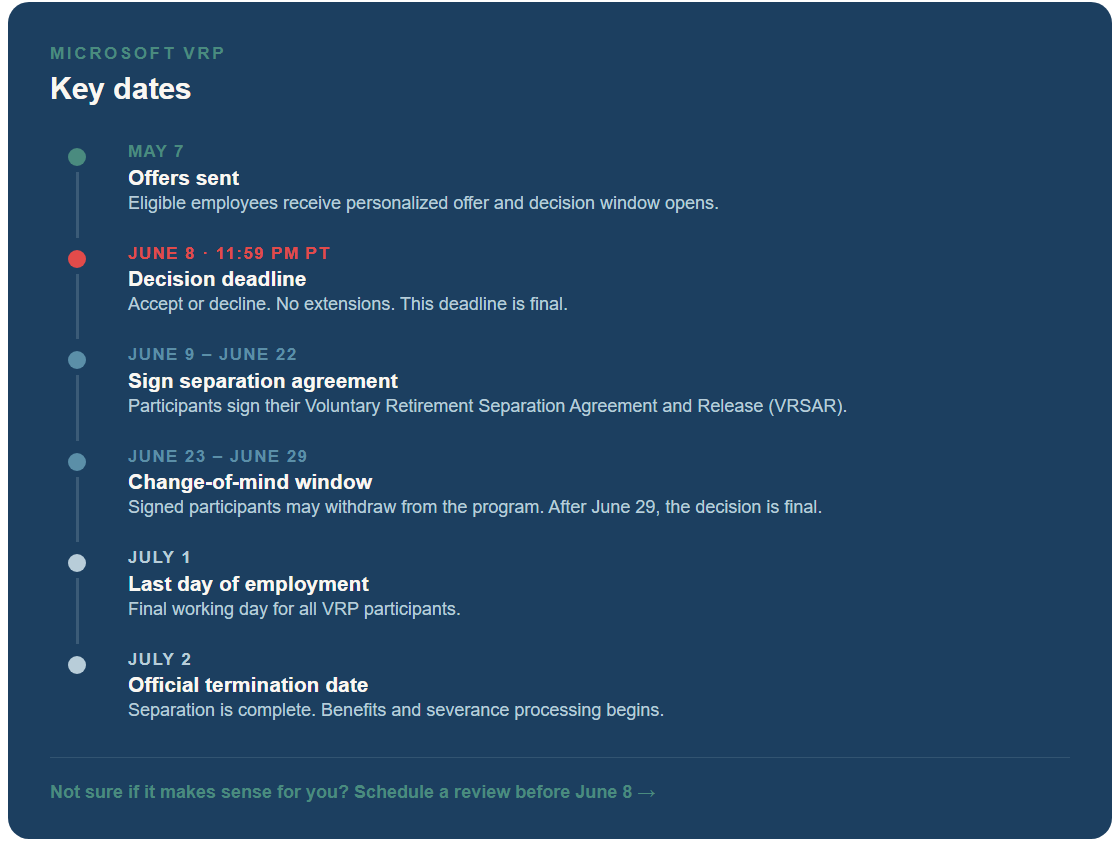

Unlike a standard layoff, the VRP is specific. It is generally open to U.S. employees at Level 67 and below whose age plus years of continuous service totals 70 or more. If you meet these criteria, you have until June 8th, EOD to decide if you will accept the offer.

The Retirement Program Components

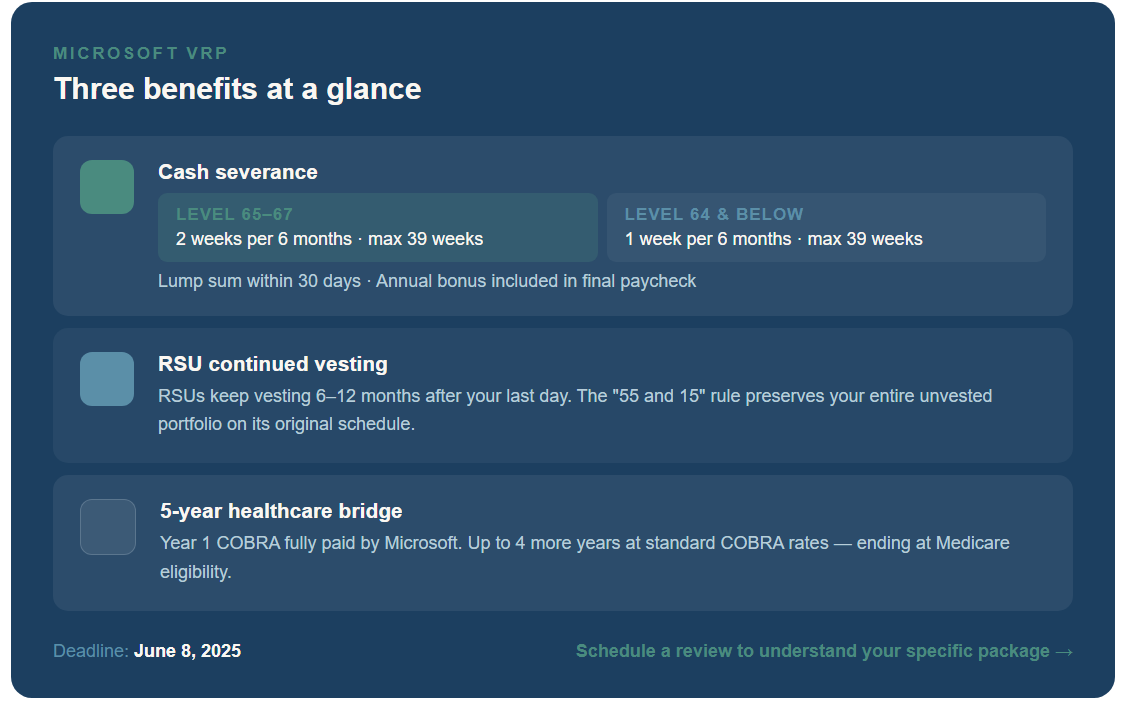

There are three main financial benefits to the VRP that should be taken into consideration.

1. Cash Severance

Microsoft is offering a lump-sum cash payout based on your level and tenure:

- Level 65–67: 2 weeks of base pay for every 6 months of service (minimum 8 weeks, maximum 39 weeks).

- Level 64 or below: 1 week of base pay for every 6 months of service (minimum 8 weeks, maximum 39 weeks).

- Annual Bonus: You remain eligible for your annual bonus, which is a critical piece of the cash-flow puzzle for a July separation.

2. RSU Extended Vesting

The VRP offers a continued vesting for your stock awards:

- Standard VRP Vest: Unvested RSUs continue to vest for 6 months after your last day.

- 24+ Years of Service: This extends to 12 months of continued vesting.

- The "55 and 15" Rule: The VRP accelerates you into this program if you are within one year of meeting the thresholds (at least 55 years old with 15 years of service or 65+ years old), allowing for the continued vesting of all eligible awards on their original schedule.

3. Extended Health Coverage

Microsoft provides a unique 5-year healthcare bridge:

- Year 1: Microsoft fully subsidizes your COBRA premiums (Medical, Dental, Vision).

- Years 2–5: You can maintain coverage for an additional 42 months at standard COBRA rates. This bridge terminates early if you reach Medicare eligibility at age 65.

Quantifying the Value: What is this worth to you?

The Cash "Bridge" If you hit the 39-week maximum, you receive roughly 75% of your annual base pay in a single check. When combined with your annual bonus, most VRP participants will see a "cash windfall" that covers nearly a full year of expenses, allowing for a smooth financial runway into the next phase of life.

The RSU "Retention Value" In a standard resignation, you leave your unvested stock on the table. Under the VRP, you could be taking 6 to 12 months of vests with you. For those bridged into the "55 and 15" program, the value is even higher with the preservation of your entire unvested portfolio.

The Healthcare "Safety Net" The first year of subsidized premiums is worth roughly $20,000–$30,000 tax-free for a family plan. More importantly, the 5-year access period protects you from the volatility of the individual insurance market, which is a major hurdle for anyone retiring before 65.

Important Considerations

- NUA (Net Unrealized Appreciation): If you hold Microsoft stock in your 401(k), the VRP separation is a "triggering event" that allows you to move that stock to a brokerage account and potentially pay capital gains tax instead of ordinary income tax. Do not roll over your 401(k) to an IRA until you check this.

- Retirement Feasibility: Just because you qualify for this offer does not mean you may be ready to retire. It is important to know your finances and have a robust retirement plan in place before accepting this offer. For those not ready to retire, there are currently no restrictions preventing you from taking the VRP and immediately starting a new job elsewhere.

- Tax Strategy: Receiving a massive severance, a bonus, and accelerated RSU vests in one year will likely push you into a higher tax bracket. Strategic planning around charitable giving or 401(k) contributions before July 1st is vital.

The Bottom Line

Microsoft is taking a $900 million charge to fund this program, and it’s likely a "one-time-only" offer. With the company forecasting further headcount reductions, the VRP is a rare opportunity to exit on your own terms with a significant financial cushion. Our firm has walked through similar VRPs with other companies like Boeing and seen it launch many successful retirements.

The most important component to this offer, is evaluating it based on the life goals that you have. Creating a good plan around your finances needs to start with your priorities.

If you would like us to evaluate your voluntary retirement offer, check your retirement feasibility, optimize tax efficiency of your retirement transition, and run a long-term cash flow analysis, schedule a meeting with us here.

Key Dates:

| Garrett Grigas, CFA, CFP® Financial Advisor & Partner

Phone: 425-902-4840 Email: Ggrigas@geverswealth.com Website: www.geverswealth.com 5825 221st Pl SE Suite 102 Issaquah, WA 98027 |