It's Almost Tax Time! What You Need – Tax Planning with President Trump in 2019

What will you need to prepare your taxes this year? Here are a few of the items that you might require from your investment accounts, and where and how you can find them.

IRA (and other qualified) accounts:

- Distributions: If you took a distribution last year, the IRA custodian will send you a form (1099R) indicating the amount. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return. Please note that Pershing may mail triplicate copies of the 1099R this year.

- Rollover or Transfer: If you did a rollover or transfer last year, this is typically a non-taxable event. The surrendering custodian, i.e. the place where the money was transferred or rolled over from, will send you a form indicating the amount. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return.

- Sales, Reinvestments, Purchases or other Re-allocations: These are typically not taxable events inside a tax-deferred account like an IRA, and you may not need or receive any tax documents regarding these.

- Roth Conversion: If you did a Roth Conversion last year, the IRA custodian will send you a form (1099R) indicating the amount. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return. Please note that Pershing may mail triplicate copies of the 1099R this year.

- IRA or Roth IRA Contribution: If you made a contribution, the IRA custodian will send you a form indicating the amount and tax year the contribution was credited for. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return.

Non-IRA/Taxable Accounts:

If you had interest or dividend income, you will receive a 1099 from the custodian in February. Please retain this form and give to your CPA for preparation of your tax return.

If you sold securities during the last year, you may need a Realized Gains/Losses Report:

- If you have an advisory (fee) relationship with us, you will automatically receive a realized gain/loss report for those accounts in the mail in February. Please retain this form and give to your CPA for preparation of your tax return. If you are on e-delivery for your statements, you can also access these reports through your dedicated web access.

- If you have a brokerage (non-advisory) account with us at Pershing, then you will receive a realized gain/loss report directly from the custodian for any sales you may have made during the course of last year. You should receive these reports by mid-February. If you are on e-delivery for your statements, you can also access these reports through your dedicated web access.

If you have an investment made many years ago, cost basis may need to be manually input. Although we will make every attempt to help document estimated cost basis, sometimes that information is not available or incomplete, especially for investments made years ago, when investment tracking software was not always as robust as current technology. Your CPA may be able to help you with lost/missing cost basis documentation.

- If you have an investment held direct at a mutual fund, the fund company will prepare and mail you a realized gain/loss report for those accounts in February. Please retain this form and give to your CPA for preparation of your tax return.

- K-1: Some investments may send you a K-1. Please see your CPA/accountant regarding proper filing of these. Please note that the investment manager will typically send K-1s to all investors regardless of what kind of investor type they are. If you receive a K-1 for an investment that you own inside a tax-deferred account like an IRA, you may not have to file that K-1 with your tax return because of the tax-deferred nature of the IRA. Professional advice from your tax-preparer is important here.

Trust Accounts

Trust accounts typically require the same information as Non-IRA/Taxable Accounts (please see above.) There may be additional reporting necessary to complete a tax return for a trust depending on the nature of that trust. We will work with your CPA to help provide any information or reports that may be required.

“The Internal Revenue Code is about 10 times the size of the Bible – and unlike the Bible, contains no good news.”

- Don Rickles

Potential Delays of 1099s:

Timely delivery of 1099s has been an ongoing problem in the custodian world. Investment custodians like Pershing have sometimes struggled to meet their January 31st mailing deadline for 1099s and sometimes even file an appeal to extend their filing date. This is especially challenging for the custodians in years which Congress passes last minute tax bills (like they have done several times in the last few years!) Watch for your 1099 from Pershing in early February – but don’t be surprised if it is a few days late. Custodians like Pershing have sometimes filed amended or corrected 1099s after sending the original 1099. We will also receive electronic copies of your 1099s in our office.

Contributions to IRAs/Roth IRAs:

If you are eligible and want to make a contribution for 2018, you have until April 15th (but please do not wait that long!) or when you file your tax return to make a contribution. Please call us if you need help with this. A note for 2019 – the contribution limit for tax payers has increased to $6,000 per year, or $7,000 if you are over 50.

Tax Planning & President Trump

One of the crown jewels of President Trump's economic agenda is drastic changes to the personal and corporate income tax rates. 2018 is the first full year of the new income tax plan. Taxpayers would be wise to understand the changes and try to adjust your financial life accordingly to try and best take advantage of the new tax plan.

Trump's proposal includes simplifying the current personal income tax code. Tax brackets, especially at the first tiers of income, are reduced by 3% or even 4%. The standard deduction is doubled and many of the exemptions and deductions for higher income tax payers are reduced or eliminated.

These new lower brackets might be especially appealing for middle to upper level tax payers, or for retirees that have the ability to control their taxable income in retirement through withdrawals from cash or non-IRA accounts. One strategy that may be especially significant under the new tax plan is partial Roth conversions up to the top of your marginal tax rate. These new lower tax rates might make partial conversions to a Roth more attractive for some tax payers. A Roth conversion strategy might help protect us and our children or heirs against future tax hikes and pro-actively draw tax-deferred income at the currently lower tax rates. Let's review this strategy and how it fits in your personal tax planning as part of our next meeting.

Big Winners under the Trump Tax plan:

- Middle & upper middle class tax-payers with no mortgage and no dependents that do not itemize.

(Doubling of standard deduction could be big tax saver.)

- Small business owners and independent contractors.

(New, potentially lower taxes for small business owners due to the QBI exemption.)

- Low income single or married

(Zero/lower tax under the Trump tax plan. My new college graduate kids are happy about this!)

- Families with estates > $12 million.

(Federal Estate tax is abolished.)

- Companies like Apple & Microsoft that have hundreds of billions of unrepatriated revenues overseas.

(May be able to bring billions back into US at a one-time reduced rate.)

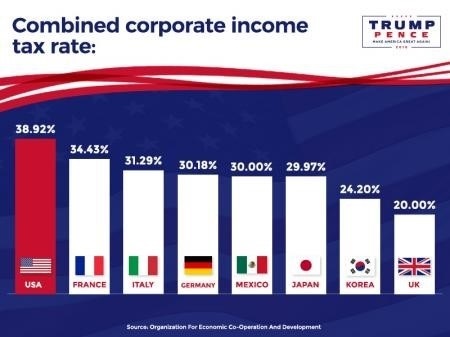

Another area of great interest is the change in corporate tax rates. Before the new tax plan, the U.S. had the highest corporate tax rate of any developed country, much higher even than the progressive socialist countries in Europe. President Trump's plan reduced that corporate tax rate to a level that is on par with the rest of the developed world and gave U.S. corporations a level playing field and incentive to keep revenues & employees inside of the United States. This has so far resulted in bringing more dollars back into the U.S. and increased U.S. tax revenues. I reviewed this in more detail in our post-election newsletter:

Trump's reduction of the corporate tax rate potentially extends to all business owners, even independent contractors, self-employed, and small business owners, through the new QBI exemption. This might have the potential to really turbocharge the small business sector. It creates additional incentive to start a business or to change one's status from employee to independent contractor. You will definitely want to review this with your CPA and see if there's an application in your own financial life if you are a small business owner or an independent contractor, or have the ability to generate independent income other than as an employee.

Economist Kevin Hassett, chairman of the American Council of Economic Advisors, was prescient when he made this prediction before the tax bill passed, as both unemployment and real wage growth are the best they have been measured in decades.

“…a country that is a friendly place to locate investment is a friendly place to work. If you think wage growth has been disappointing since the recovery began, you should pop the champagne cork when this becomes law.”

- Kevin Hassett

It is an exciting time for tax planning. We look forward to working with you and your CPA and reviewing tax planning ideas in more detail at our next meeting.

Tax Planning Strategies

There have also been some new changes in the last years that may be worth exploring to see if they may be relevant to your personal financial circumstances. Here are a just a few:

IRS Approval of Split Rollovers from 401(k) to IRA and a Roth IRA

The IRS will now allow a rollover from an employer-sponsored retirement account (like a 401(k)) to be treated as a single distribution, even if it contains both pre-tax and after-tax contributions, and furthermore that distribution can be rolled over into separate accounts. So, a 401(k) owner can rollover their before tax portion into their IRA account and their after-tax portion into a Roth IRA, allowing them to try and maximize their future earnings potential in the most tax-efficient manner.

A retiring 401(k) holder will definitely want to check and see if they can take advantage of this favorable tax strategy. A current 401(k) holder may want to consider additional after-tax contributions to their plan as they now may be able to rollover those contributions to a Roth IRA in the future – effectively giving a high-income executive a back-door method to contribute significant amounts of money to tax-friendly Roth accounts. (This Forbes article covers some more of the technical details of this strategy. https://www.irahelp.com/slottreport/backdoor-roth-conversion

Consult with your tax advisor for specifics and guidance regarding your personal situation.)

Employees of companies that offer after-tax contributions, like Microsoft for example, could potentially rollover those after-tax amounts into a Roth IRA after they separate from the company – effectively giving even very high-income upper executives the ability to create large pools of tax-free capital for their future retirement enjoyment.

Trusts for IRAs for Creditor and Inheritor Protection

A recent Supreme Court ruling clarified that non-spousal inherited (Stretch) IRAs do not enjoy creditor protection like other IRAs or 401(k)s do. This makes trust planning for inherited IRA assets even more important than before.

If your children have financial challenges, or if they might be subject to risk of creditors and lawsuits, it may be smart to consider if a trust strategy makes sense for your IRA account. Savvy families often set up a trust specifically to receive larger IRA accounts after they are gone, with the goal and intent being to provide lifetime income for their children and protect them from making bad money decisions.

Department of Labor and SEC Regulations for IRAs and Retirement Accounts

The Department of Labor (DOL) and SEC are still debating and discussing additional new comprehensive regulations for IRAs and other retirement accounts.

We may want to watch these potential regulations and review if your IRA and other retirement accounts might require any changes that we should consider. Some legal experts believe that the direction of the new rules will have the consequence of strongly encouraging IRA portfolios to move to no-load index funds and exchange traded funds (ETF’s) – a service we have been using and offering for quite some time. We can review this subject in-depth with you at our regular review appointments.

Life Income Annuities Now Approved for Retirement Accounts

The IRS finalized regulations allowing qualified longevity annuity contracts (QLAC) in retirement plans. A QLAC is a type of annuity contract that is purchased within a retirement plan and that pays guaranteed annual income at a desired age, typically during retirement. An interesting twist is that a QLAC is excluded from the retirement account’s value when calculating the client’s required minimum distributions (RMDs) after the client reaches age 70 ½. Because of this exclusion, a QLAC might be a tax reduction strategy to consider if you do not need income from your IRA but are still required to take it because you are over age 70.

IRS Permanently Allows Charitable Gifts from IRA Accounts for IRA Owners over 70

Congress reauthorized the IRA charitable rollover and made it permanent. IRA owners aged 70 ½ and older may transfer up to $100,000 from their IRA to a qualified public charity. The transfer will be made free of federal income tax, and the gift also qualifies for the donor's required minimum distribution (RMD).

Charitable gifts made directly from an IRA account:

- May be used to satisfy Required Minimum Distribution (RMD) requirements

- Can be an income tax planning tool

- Might reduce Adjusted Gross Income (AGI)

- Are an efficient way to make charitable gifts

Many of our clients have used this provision to generously support churches, community groups and other charities that are doing charitable work that is important to them. You may want to consult with your CPA or tax advisor to see if this might make sense in your personal situation.

Taxes and Your IRA Accounts

The projected government budget shortfall (the deficit) for 2018 was over $800 billion dollars – over TRIPLE what it was in 2002. Worse yet, our National Debt has passed $22 trillion.

Please understand, I’m not trying to stir a hornet’s nest of political debate or democrat vs. republican strife. Whatever your political persuasion, there is wisdom to be drawn from this observation for all investors. The government is in trouble, and if it gets worse, they are likely to try and eventually solve their problem by collecting even more taxes from me and you. One of the largest potential sources of additional government tax revenues are our tax-deferred IRA accounts.

As many of our clients have retired or are retiring from successful executive careers, they typically have large retirement account balances. These tax-deferred accounts might be in the cross hairs of future increased taxation, and we might be wise to carefully consider how we use these accounts.

Some tax strategies for larger IRA accounts that might be appropriate may include:

- Filling up marginal tax brackets with additional withdrawals (this is especially significant under the new Trump tax plan!)

- Combining qualified and non-qualified capital to draw income in a most tax-efficient manner

- Partial Roth IRA conversions

- Charitable RMDs

- Charitable testamentary beneficiary designations

- “Stretch” IRAs

and others.

Let’s discuss tax planning for 2019 at our next review meeting and try to identify any strategies or changes that might be suitable for your personal situation – especially as it may relate to large IRA accounts.

Our tax burden may get worse if the government budget shortfall worsens in the future. Investors and retirees may be wise to pay attention to tax planning and be alert and aware of strategies that might minimize tax pain for you and for your family.

"I'm proud to be paying taxes in the United States. The only thing is – I could be just as proud for half the money."

- Arthur Godfrey

Snow, Snow, and More Snow!

On a personal note, we hope you made it through last month’s snow apocalypse without too much damage. We all dealt with it in our own manner here at the office. Kristy had over three feet at their home in North Bend and could not even open her front door for several days, Garrett bravely walked to work early each morning, Barbara worked from home in Woodinville to avoid the icy roads, and Anna & Gabrielle – who each work remotely from Alaska and Spokane respectively – laughed and jeered at the wimpy Seattleites! One of our dear clients even took pity on us and knit the whole office warm and very cool hats – thanks Joanie ?

My wife and I took full advantage of the unique weather for a snowshoeing adventure with some friends and business associates.

It was a grand adventure while it lasted, but we are all, as I’m sure you are, looking forward to spring and sunshine.

Returning again to April and tax time – please know that we are committed to helping you any way that we can to complete your tax return, and please feel free to call us for any help or clarification. We also welcome calls from your CPAs and tax-preparers, and with your permission can provide them with information they need for your tax return.

We purposely keep our schedule light in late March and April to be as responsive to our clients as we can, however, it does tend to get very hectic by April, and if you delay your request for information until then, it may take a while for us to respond, or perhaps you may consider filing an extension.

Thanks for your trust and relationship. We remain committed to your financial well-being.

Warm Regards,

Willy Gevers

PS: We have been repeatedly asked by clients if they could share these e-mail notes with their friends or neighbors. Please feel free to forward this with the stipulation that it may only be forwarded if done so in its entirety with no portions omitted. We would be delighted to share our comments and opinions with your friends and welcome your comments and feedback.If you received this and would like to be included on our newsletter list, please email us at info@geverswealth.com