It’s Almost Tax Time... Major Tax Changes Coming, are you Prepared?

Winter 2022

2022 may be a year of big tax changes. Congress is busy writing new legislation that may impact all of us – and probably not in a good way. Let’s review some of these possible changes...but before we do let’s make sure we are ready to file our 2021 taxes.

What will you need to prepare your taxes this year? Here are a few of the items that you might require from your investment accounts, and where and how you can find them.

IRA (and other qualified) accounts:

-

Distributions: If you took a distribution last year, the IRA custodian will send you a form (1099R) indicating the amount. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return. If you are a seasoned investor, please remember that the new age to start your RMD is age 72 (it was formerly 70 1/2.)

-

Rollover or Transfer: If you did a rollover or transfer last year, this is typically a non-taxable event. The surrendering custodian, i.e., the place where the money was transferred or rolled over from, will send you a form indicating the amount. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return.

-

Sales, Reinvestments, Purchases, or other Re-allocations: These are typically not taxable events inside a tax-deferred account like an IRA, and you may not need or receive any tax documents regarding these.

-

Roth Conversion: If you did a Roth Conversion last year, the IRA custodian will send you a form (1099R) indicating the amount. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return. We helped client implement many Roth conversions in 2021 because of the proposed tax changes.

-

IRA or Roth IRA Contribution: If you made a contribution, the IRA custodian will send you a form indicating the amount and tax year the contribution was credited for. You should receive this in the mail in February. Please retain this form and give to your CPA/accountant for preparation of your tax return.

Non-IRA/Taxable Accounts:

If you had interest or dividend income, you will receive a 1099 from the custodian in February.

Please retain this form and give to your CPA for preparation of your tax return.

If you sold securities during the last year, you may need a Realized Gains/Losses Report:

-

If you have an advisory (fee) relationship with us, you will automatically receive a realized gain/loss report for those accounts in the mail in February. Please retain this form and give to your CPA for preparation of your tax return. If you are on e-delivery for your statements, you can also access these reports through your dedicated web access.

-

If you have a brokerage (non-advisory) account with us at Pershing, then you will receive a realized gain/loss report directly from the custodian for any sales you may have made during the course of last year. You should receive these reports by late February (but see my notes on Internal Revenue delays below!) If you are on e-delivery for your statements, you can also access these reports through your dedicated web access.

If you have an investment made many years ago, cost basis may need to be manually input. Although we will make every attempt to help document estimated cost basis, sometimes that information is not available or incomplete, especially for investments made years ago, when investment tracking software was not always as robust as current technology. Your CPA may be able to help you with lost/missing cost basis documentation. -

If you have an investment held direct at a mutual fund, the fund company will prepare and mail you a realized gain/loss report for those accounts in February. Please retain this form and give to your CPA for preparation of your tax return.

-

K-1: Some investments may send you a K-1. Please see your CPA/accountant regarding proper filing of these. Please note that the investment manager will typically send K-1s to all investors regardless of what kind of investor type they are. If you receive a K-1 for an investment that you own inside a tax-deferred account like an IRA, you may not have to file that K-1 with your tax return because of the tax-deferred nature of the IRA. Professional advice from your tax- preparer is important here.

Trust Accounts

Trust accounts typically require the same information as Non-IRA/Taxable Accounts (please see above.) There may be additional reporting necessary to complete a tax return for a trust depending on the nature of that trust. We will work with your CPA to help provide any information or reports that may be required.

“The Internal Revenue Code is about 10 times the size of the Bible – and unlike the Bible, contains no good news.”

- Don Rickles

Potential Delays of 1099s & Delays at the Internal Revenue Service:

Timely delivery of 1099s has been an ongoing problem in the custodian world. Investment custodians have sometimes struggled to meet their mailing deadlines for 1099s and sometimes even file an appeal to extend their filing date. This is especially challenging for the custodians in years which Congress passes last minute tax bills (like they have done several times in the last few years!) Watch for your 1099 from Pershing in February – but don’t be surprised if it is a few days late. Custodians like Pershing have sometimes filed amended or corrected 1099s after sending the original 1099. We will also receive electronic copies of your 1099s in our office.

To make matters worse, the IRS is severely behind and apparently woefully understaffed because of the widespread labor shortage. As of year-end they still had over 6 million unprocessed returns, and Treasury officials warned of, “enormous challenges during this year’s tax filing season, which will cause delays to refunds and other taxpayer services.”

Additionally, prominent CPA Ed Slott is on record saying, “Review Form 1099s, as they can be rife with errors. We’re finding there are lots of mistakes in there — maybe some of these institutions were short-staffed or people were working from home ..., he explained. “You type the wrong code into a 1099-R for retirement distributions, it can make the difference as to whether something is taxable or not or subject to a penalty. Due to COVID-19 we are seeing more mistakes on the 1099s this year.”

I would note that we have seen errors in Qualified Charitable Distributions (QCD’s) on client’s tax returns over the last several years. You may want to ask your CPA to double-check QCD status on your 2021 return (if you made a QCD last year.)

Contributions to IRAs/Roth IRAs:

If you are eligible and want to make a contribution for 2021, you have until April 18th (but please do not wait that long!) or when you file your tax return to make a contribution. Please call us if you need help with this. A note for 2022; the contribution limit for taxpayers has not changed and is the same as it was in 2020 at $6,000 per year, or $7,000 if you are over 50.

“Worried about an IRS audit? Avoid what’s called a “Red Flag.” That’s something the IRS always looks for. For example, say you have some money left in your bank account after paying taxes. That’s a Red Flag!”

- Jay Leno

Our whole team is ready to help you and your CPA with your 2021 tax preparation, and of course please feel free to call us if we can help in any way.

Tax Hikes?

Congress is proposing numerous tax changes, especially because of the proposed “infrastructure” bill, and the need to fund it. We follow and read several tax attorneys and tax specialists, and if and when tax law changes, we will analyze them, as well as any strategies to try and mitigate or avoid new or higher taxes. We can review these with you at our review meetings and this may be an important part of our meeting agendas for this year.

Some of the changes that have been discussed include:

-

- Elimination of the “back-door” Roth IRA conversion for high income taxpayers.

-

- Increase of the capital gains & dividend rate for higher income taxpayers.

-

- Increase of the Net Investment Income Tax for high earning self-employed business owners.

-

- Change in gain recognition by trusts of appreciated and otherwise untaxed gains.

-

- An additional surtax on high income taxpayers

-

- A penalty/excise tax for very large IRA accounts

-

- (And perhaps lots of other unpleasant surprises.)

Congress hopes to pass tax increases to fund spending bills. However, the closer we get to the mid- term elections in November, the less likely tax increases are to pass, as that becomes a strong negative to voters.

On a friendlier note, the SECURE 2.0 Bill is gathering bi-partisan support and seems likely to pass in some form. Possible changes include:

-

- RMD’s move to age 75 (now 72)

-

- Indexing the catch-up contribution for inflation

-

- Greater catch-up contributions to 401(k) and other retirement plans for investors 62 and over.

-

- SIMPLE and SEP plans both allowed.

-

- Employer matching contributions to Roth Plan accounts.

Reducing and or/avoiding taxes becomes increasingly more valuable and significant the higher tax rates are, and the more complex the tax code becomes. We work closely with our client’s CPAs to try and look for strategies to lessen tax burdens.

We frequently help our clients analyze and implement tax-efficient portfolio distribution strategies, tax-loss harvesting and tax-efficient portfolios, Roth conversions, optimization of company Qualified and non-Qualified plans, and Medicare Means threshold planning. We also are familiar with using trusts in tandem with income tax strategies, with charitable tax strategies, both current and deferred, and with stock options and timing and selling and exercise strategies – again all with the goal of reducing or avoiding taxes.

And, our whole team gets excited about finding ways to help our clients become better off!

We keep our schedule flexible during tax season so we can be available to help our clients and their CPA’s. Please feel free to reach out to us if we can help in any way with your 2021 tax return preparation.

We look forward to seeing you soon for your next review meeting.

Warm regards,

Willy Gevers

PS: We have been repeatedly asked by clients if they could share these e-mail notes with their friends or neighbors. Please feel free to forward this with the stipulation that it may only be forwarded if done so in its entirety with no portions omitted. We would be delighted to share our comments and opinions with your friends and welcome your comments and feedback. If you received this and would like to be included on our newsletter list, please email us at info@geverswealth.com

Copyright 2022 William R. Gevers. All rights reserved.

Gevers Wealth Management, LLC

5825 221st Place SE, Suite 102

Issaquah, WA 98027

Office: 425.902.4840

Fax: 425.902.4841

Email: info@geverswealth.com

Website: www.geverswealth.com

The views are those of Gevers Wealth Management, LLC, and should not be construed as individual investment advice. All information is believed to be from reliable sources; however, no representation is made as to its completeness or accuracy. All economic and performance information is historical and not indicative of future results. Investors cannot invest directly in an index. Please consult your financial advisor for more information. This material is designed to provide accurate and authoritative information on the subjects covered. It is not, however, intended to provide specific legal, tax, or other professional advice. For specific professional assistance, the services of an appropriate professional should be sought. Past performance is not indicative of future results. All investing involves risk, including the potential for loss. No strategy can ensure a profit or protect against loss in a declining market. Securities and advisory services offered through Cetera Advisor Networks LLC Member FINRA/SIPC a broker/dealer and a Registered Investment Advisor. Cetera is under separate ownership from an any other named entity.

US Money Supply, US Dollar, Inflation/Deflation, Debt Watch

"Neither a wise man nor a brave man lies down on the tracks of history to wait for the train of the future to run over him."

- Dwight D. Eisenhower

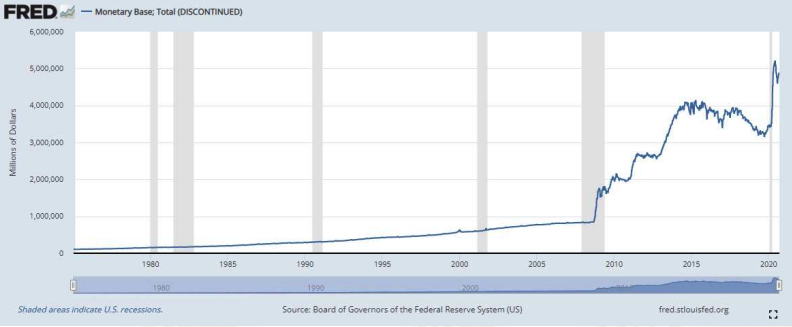

US Money Supply –Monetary Base

(https://fred.stlouisfed.org/series/BOGMBASEW)

US Dollar Price – (DXY) USD Index measured against other currencies

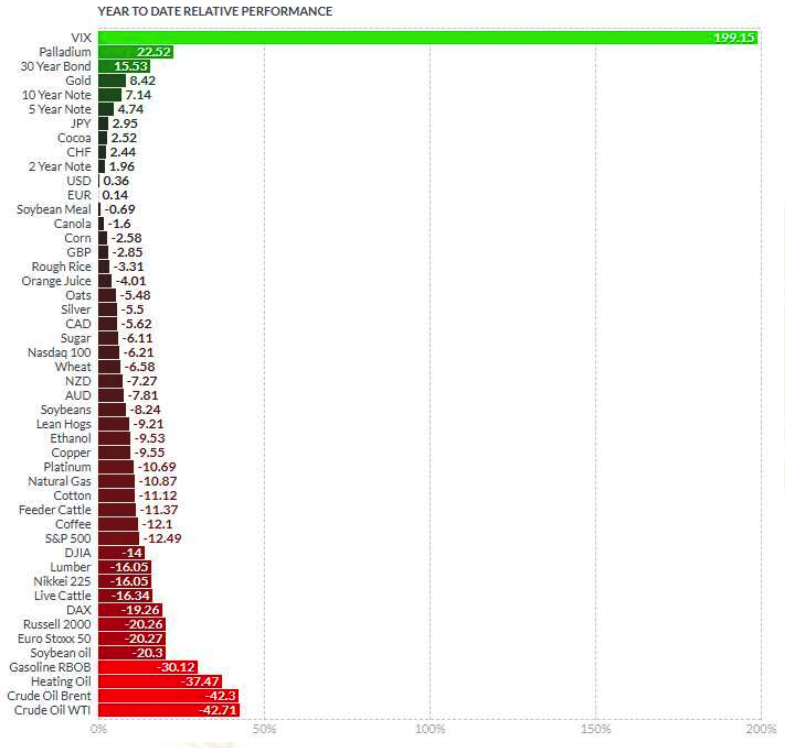

Inflation/Deflation:Year to Date price change in commodities as measured by futures

(http://www.finviz.com/futures_performance.ashx?v=17)

Velocity of Money – Velocity is a measure of how quickly money is spent. High velocity is typically a precondition for inflation.

(http://research.stlouisfed.org/fred2/series/MZMV)

Debt

Tracking US Debt Levels - remember that increasing debt levels generally push up asset prices; stocks, real estate, and other investments. Eventually, debt levels will need to be reduced, or else we'll reach a point where extreme monetary fiscal policy must be taken if the debt reaches unsustainable levels. A family that lives beyond their means for too long and goes deeply into debt may end up in financial ruin. A country that goes too deeply into debt for too long may also have to have a day of reckoning.

“Let no debt remain outstanding, except the continuing debt to love one another, for whoever loves others has fulfilled the law.”

- Paul

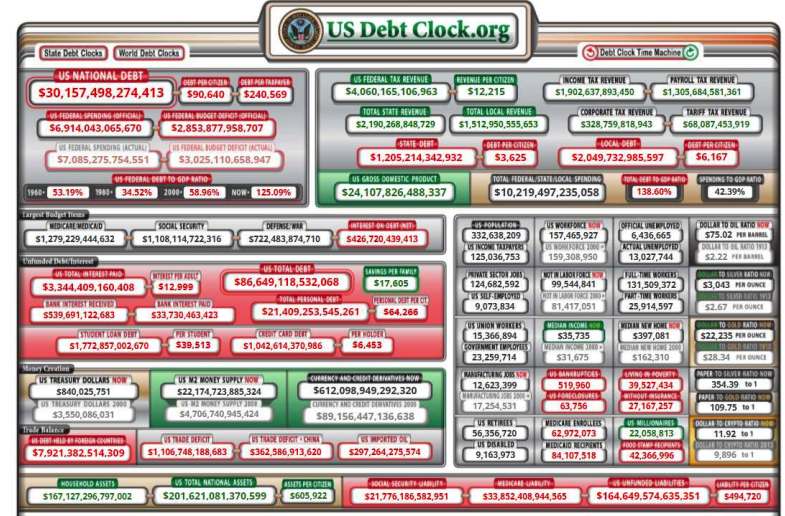

Total US Debt

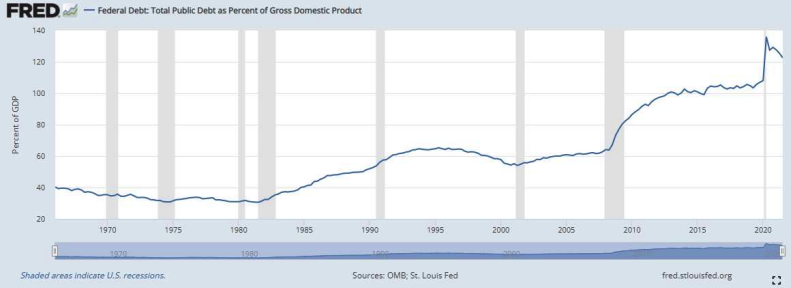

US Debt to GDP Ratio

(note: ratio of US Federal Debt to Gross Domestic Product. Ratios >100% are unusual and considered economically unhealthy. https://fred.stlouisfed.org/series/GFDEGDQ188S )

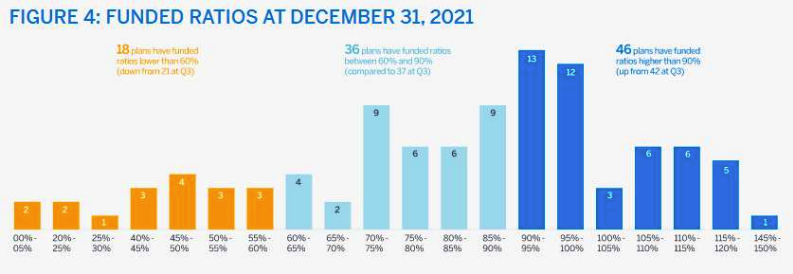

Pension to Liabilities Chart – Public Pensions

(note: 100% funding means that the pension plan has enough assets to pay its projected retirement benefits.)

http://www.milliman.com/ppfi/

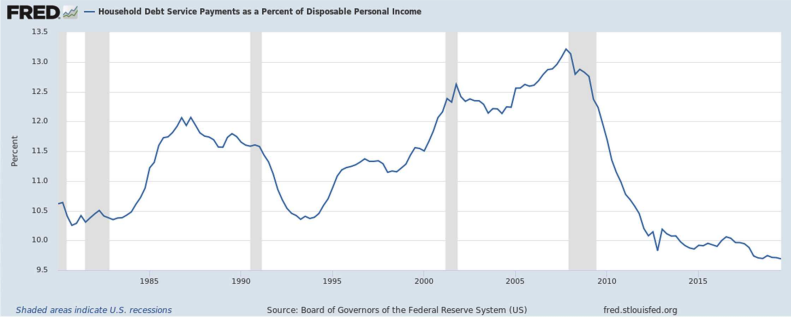

Household Debt Payments as a Percentage of Personal Income

(Note: the lower the ratio – the better that households are able to make their loan payments.)

https://fred.stlouisfed.org/series/TDSP

https://www.thinkadvisor.com/2022/02/16/ed-slotts-tax-season-game-plan-for-advisors/ https://www.thinkadvisor.com/2021/12/22/prep-your-clients-for-2-bills-that-could-change-iras-in-2022-ed-slott/