I Read the News Today, Oh Boy … the Candidates, your Investments & Paul McCartney

Have been following the presidential candidates debates with great interest – not because of politics, but because of how each of the leading candidates’ platforms and positions might impact the investment markets.

Before we go any further – I often and emphatically like to state that we try to be agnostic about politics in our meetings and try to keep the focus and discussion on our investments and the markets and ignore ideology. We have a great deal of affection for all of our clients, whose political beliefs range across the spectrum, and we can keep better relationships and try and give better advice if we can avoid getting enmeshed in polarizing politics.

So with that caveat, let’s dive into policy and the markets.

The Markets Hate Uncertainty – What about a new President?

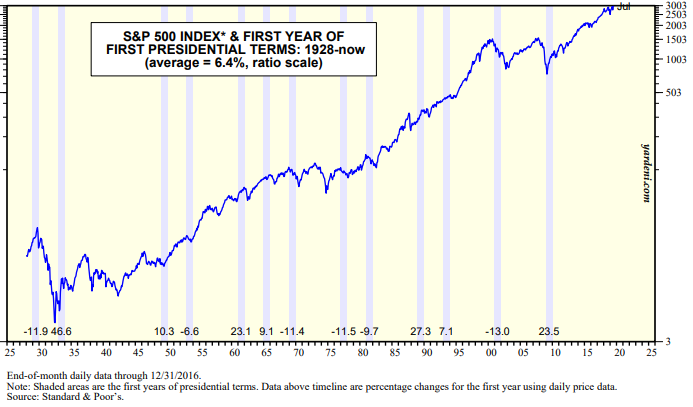

Uncertainty is bad for the stock market. You have probably heard that wall street proverb many times, and there certainly seems to be some truth to that. But how does the uncertainty of the possibility of a new president impact the markets?

According to history – a new president is not necessarily a bad thing, at least as far as the stock market is concerned. Our last two presidents have been about as far apart ideologically as one could imagine, but the first year returns of each were quite good. President Obama’s first year in 2009 the US stock market reported a 26.5% annual return, and in President Trump’s first year in office in 2017 the US stock market was up 21.94%.

From 1928 until today, the average stock market return during the first year of a president’s term has been a little over 6% per year, slightly below the long-term average but not that bad of a return!

(Notice that although the average is positive, there have been a number of cases where the markets were negative during that first presidential year.)

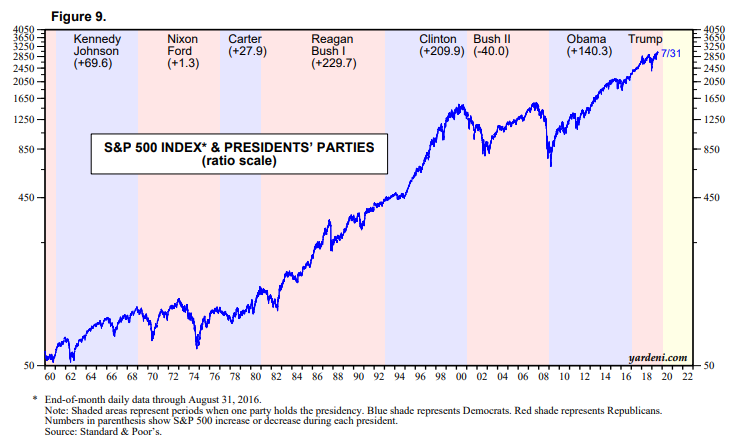

Stock Market Returns & Democrats vs. Republicans

But what about Democrats vs, Republicans? We all seem to have a party that we are loyal to – but the US stock market seems to like both parties, as the returns during both D and R presidencies have been generally good as the following graph shows.

It is encouraging to us as investors that the markets have done well under both parties. So what then should we be watching?

Policies are Levers

The leading democratic challengers to President Trump all have very substantial “give aways” as a prominent part of their platforms. These policies are like levers that if enacted have the power to sway stock, bond, commodity markets and interest rates and thus potentially impacting our portfolios.

Let’s examine the four current front runners, Warren, Harris, Sanders and Biden and their stated platforms:

Elizabeth Warren – Healthcare for all, Abolish Private Insurers

Harris – 100 Billion for black home ownership

Sanders – also wants to cancel all student loan debt

Biden – Greatly expanded Health Care

Warren, again – Break-Up of Big Tech Companies

The race is very early, and the outcome is unclear – but what is clear is that if one of the current leading democratic challengers ends up as our next president, the current economic policies of the US Government will change dramatically.

Some questions we may consider in 2020 as the election coalesces, and we find out who wins.

If President Trump does not get re-elected, and we have the economic uncertainty of a new president, should we re-consider risk levels in our investments?

What sectors and companies might benefit from these policies? (paying off all college debt, Medicare for all, eliminating private insurance, Breaking up Tech companies, etc.)

Which sectors and companies might be hurt from these policies?

What is the possible impact on interest rates and bonds because of increased government entitlements and give aways?

What are the possible impacts on commodities of some of these policies?- and how might the Federal Reserve act?

Here is a small recent example of presidential politics impacting policies and thus investment markets. The Fed chair Jerome Powell has been harangued by President Trump to shift interest rate policy. After weeks of rumors, the Fed just announced a rate decrease. Consequently, the price of Gold (which has been basically flat for about 6 years) zoomed up about $200 per oz.

It is quite possible that the policies and promises of the democratic front runners, if enacted, might have even more profound impact than this relatively minor example.

Next year might certainly provide a good opportunity for us to re-evaluate our portfolio and sector allocations, our risk levels, and our personal investment income needs and cash & liquidity requirements.

Stay cheerful as an investor – no matter which party you hold allegiance to. The miracle that is the United States economy has rewarded long-term investors through both democrat and republican led periods, even back to our grandparent’s lifetimes. Let’s expect and believe that long term historical trend will continue.

Speaking of government policies, here is another potential regulatory change that might have a dramatic impact on how we plan for our IRA’s.

SECURE Act of 2019 – Great for Many, but Painful for Beneficiaries of Larger IRA’s

The House recently and overwhelmingly passed the SECURE Act, ‘Setting Every Community Up for Retirement Enhancement Act of 2019, and it is expected that the Senate will soon do the same. The bill contains some wonderful provisions that have the goal of encouraging and enhancing Americans ability to achieve retirement security. However it also changes current laws.

The SECURE Act of 2019 (if enacted into law) would eliminate the current rules that allow non-spouse IRA beneficiaries to "stretch" required minimum distributions (RMDs) from an inherited IRA account over their lifetimes (which would potentially allow the IRA to grow tax-free for decades). Instead, the inherited IRA would have to be distributed to non-spouse beneficiaries within 10 years of the IRA owner's passing (with some exceptions).

Translation – if you have a larger IRA or 401k account, your children and grandchildren will have just lost a planning strategy that might have helped them avoid huge amounts of income taxes!

We have been studying the SECURE Actof 2019 with the anticipation that it will probably become law. Many of our clients have seven figure plus IRA and/or 401(k) balances. If this legislation passes, it may require a whole new strategic review of tax strategies and planning options. We will write more about the SECURE Act if it does becomes law, and it will certainly be an important topic of future review meetings.

Paul McCartney & The Beatles

"Being in the audience actually looks quite a bit of fun." - Paul McCartney

If you didn't catch the musical allusion -- I read the news today; oh, boy - is a lyric from A Day in the Life, a Beatles song. My wife, son, and I all love classic rock. If you walk by our home on any summer night, you might hear a trio of out of tune voices singing along with a Beatles song! Our family recently saw The Beatles movie, Yesterday, and greatly enjoyed it. We have been listening to Beatles music almost nonstop ever since.

And then to top it off, youngest son Trey and I celebrated our birthdays with an incredible concert. Ringo Starr joined Paul McCartney during the encore and played several songs. A hundred thousand people in Dodger’s Stadium went nuts as we witnessed the closest you can get to a Beatles reunion.

BTW - listening to the music I realized that the Beatles had a lot to say about money and taxes in their songs. We may be writing more about that in future client newsletters.

Yes it was - Thanks Sir Paul, and Happy Birthday Trey!

"Though I know I'll never lose affection, for people and things that went before, I know that I'll often stop and think about them. In my life, I'll love you more." In My Life

Best wishes for a great summer. We look forward to seeing you again for your next review meeting.

Warm Regards,

PS: We have been repeatedly asked by clients if they could share these e-mail notes with their friends or neighbors. Please feel free to forward this with the stipulation that it may only be forwarded if done so in its entirety with no portions omitted. We would be delighted to share our comments and opinions with your friends and welcome your comments and feedback.If you received this and would like to be included on our newsletter list, please email us at info@geverswealth.com

Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing.